Creating Louisiana’s Operating Budget: A Primer

This week the governor will unveil his recommended budget to the legislature and the public. The Joint Legislative Committee on the Budget (JLCB) will meet during its regular monthly meeting to discuss it and address other regular business items. This creates an opportune time to discuss how Louisiana’s operating budget is developed.

The process of funding state government operations is the most significant means by which the policy and direction of state government are established. The state constitution provides guidelines for the process in that it:

- Requires a balanced budget, so expenditures do not exceed the revenue.

- Limits the growth of the budget from year to year.

- Requires that debt payments are made before any other spending in the budget.

- Restricts the uses of revenue that will not be available in future years.

- Requires economic experts to arrive at a consensus when forecasting revenue to provide more realistic estimates.

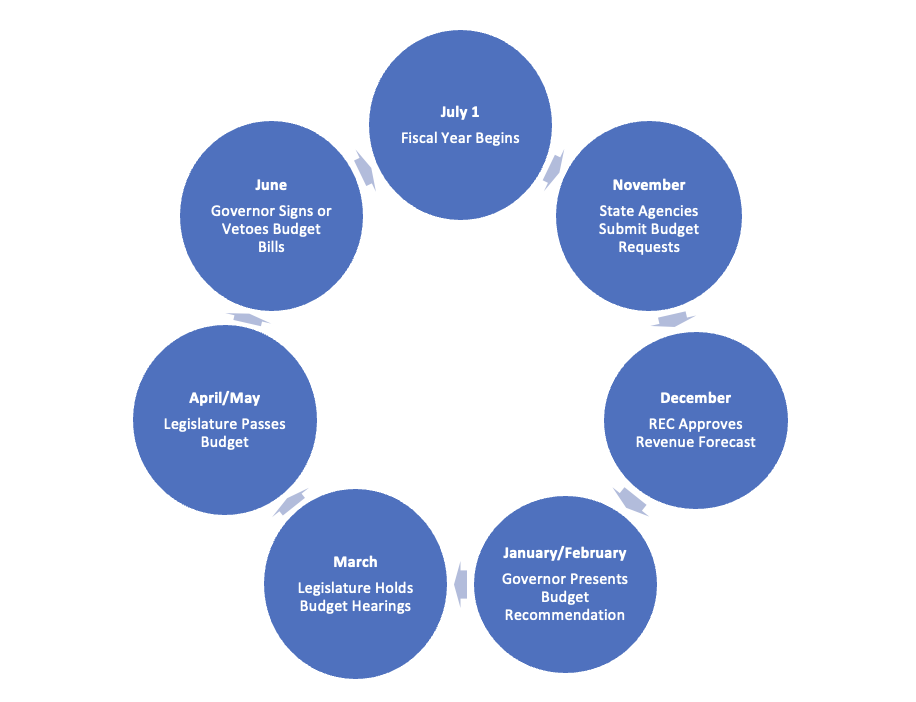

Like most states, Louisiana uses an annual operating budget with a fiscal year that runs from July 1 to June 30. Therefore, a budget must be in place before July 1st each year for state government’s orderly and consistent operation. The process of developing and implementing that budget takes much longer and requires the involvement of both the executive and legislative branches.

The process comprises three phases: agency budget development, enactment (approval) through the legislative process, and execution guided by the governor with oversight by the legislature.

The governor must develop and recommend an annual operating budget each year before the legislative session. But before this can occur, each executive branch department or state agency must submit a budget request. This request includes a comparison of actual expenditures from the prior year, the operating budget that is already in place, and each request for the upcoming year. These requests include all items that are currently in the budget at the estimated cost to continue into the following year, plus any additional or expanded programs or activities planned for the following year.

With the assistance of the Commissioner of Administration and his staff in the Office of Planning and Budget, the governor can decide which currently funded items to include in the next budget and any new items to include. This becomes the executive budget that is then recommended to the legislature.

However, before the governor can recommend a budget, the Revenue Estimating Conference (REC) must meet to establish and approve the annual revenue forecast. REC comprises the governor, a university economist, the Speaker of the House, and the President of the Senate. This group receives two forecasts from which to choose. They are provided by a legislative staff economist and an economist from the executive branch. At no point can the budget ever exceed this forecast.

These recommendations become a series of appropriations bills:

- General Appropriations Bill, or House Bill 1, provides for the annual operating budgets of state executive branch agencies.

- Capital Outlay Bill (HB 2) provides for multi-year, large-scale capital projects.

- Ancillary Appropriations Bill provides for the revolving fund and other appropriations for “back-office” functions such as technology services, insurance, and procurement.

- Legislative and Judicial expense bills that appropriate funds for the regular operations of those separate branches of government.

- Funds bill transfers money from one account of dedicated funds (legally earmarked for a specific purpose) to another or from the state’s general fund to a dedicated account of funds.

- Supplemental bill funds unanticipated government expenses in the current fiscal year using any excess money that may be available or making cuts to the budget in times of revenue shortfall.

- Non-appropriated requirements constitute a portion of the budget created before any other priority is appropriated. It does not require a bill or legislative approval to spend these funds. They are taken off the top before the budget process even begins. These funds are used to pay the annual payments on the state’s debt. The state acquires debt primarily through the capital outlay process, which provides funding for capital-intensive projects.

With its own budget staff, the legislature approves or changes the governor’s recommended budget through the legislative process. Once the budget is approved, both the executive and legislative budget staff monitor expenditures throughout the year.

The JLCB, comprised primarily of House Appropriations and Senate Finance Committees members, meets each month throughout the year to monitor the budget, authorize changes, and conduct oversight hearings for any fiscal-related subject. Executive staff can authorize any minor changes to the budget unilaterally, but major changes can only occur with the legislature’s approval through the JLCB. In addition to the balanced budget limitation, the constitution also provides for an expenditure limit. Unlike the federal government, the state budget can never exceed revenue.

While all of this may seem terribly complicated, these processes and rules help to create a fiscal policy that should mirror how Louisiana families budget and use their own dollars, adhering to the basic principles of:

- Don’t spend more than you earn.

- Live within your means.

- Don’t pay your regular expenses with one-time money.

- Pay your debts first. And save for the future.

And because the state budget is taxpayer-funded, lawmakers add to this list to maintain transparency to the public.

It will be interesting to see what the governor sets as his top fiscal priorities for his final year in office and equally interesting to see if the legislature agrees with those priorities when two-thirds of them are up for re-election later this fall.